Artificial Intelligence Chip Market Growth: AI Workloads, Semiconductor Innovation & Forecast to 2034

Rapid digital transformation, increasing enterprise AI adoption, and rising demand for energy-efficient processors are accelerating technological advancement in the artificial intelligence chip market.

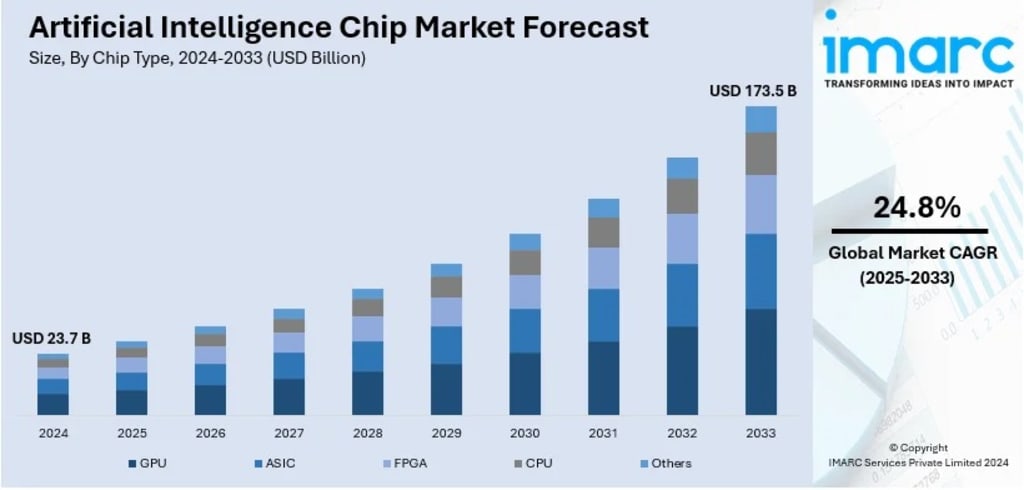

Rapid advances in machine learning, surging demand for cloud infrastructure, and the explosive growth of generative AI are driving unprecedented demand for AI chips worldwide, supported by rising enterprise AI adoption, government-backed semiconductor initiatives, and deepening integration across automotive, healthcare, and consumer electronics. According to IMARC Group’s latest data, the global artificial intelligence chip market size was valued at USD 23.7 Billion in 2024. Looking forward, IMARC Group estimates the market to reach USD 173.5 Billion by 2033, exhibiting a CAGR of 24.8% during 2025–2033. North America currently dominates the market, holding a market share of over 32.1% in 2024.

Get a Sample Report for Actionable Market Insights

The AI chip market has evolved from a niche GPU-driven segment into a broad, high-stakes technology battleground. Today’s demand is shaped by the race to build faster, more efficient processors for large language models, real-time inference, and edge AI deployment. Key chip types include GPUs, ASICs, FPGAs, and CPUs, with ASICs commanding around 34.3% of market share in 2024 due to their purpose-built performance advantages. System-on-Chip (SoC) technology leads by architecture at 48.8%, while edge processing accounts for 63.6% of demand by processing type — reflecting a decisive shift toward localized, low-latency computing. Healthcare tops the industry vertical rankings at 19.9%, with automotive, BFSI, and IT and telecom all expanding rapidly. Natural Language Processing leads the application segment at 28.2%, powered by the global proliferation of chatbots, virtual assistants, and voice-driven platforms.

Get a Sample Report for Actionable Market Insights

Artificial Intelligence Chip Market Growth Drivers:

● AI-Powered Automotive and Mobility Revolution

The automotive sector is one of the most powerful demand engines for AI chips today. Advanced Driver Assistance Systems (ADAS), autonomous driving features, and in-car infotainment all require chips capable of processing enormous sensor datasets in milliseconds. In 2024, Intel demonstrated AI-enhanced SDV SoCs running 12 simultaneous workloads — including generative AI, e-mirrors, and video conferencing — on a single platform. As automakers aggressively target Level 3 and Level 4 autonomy, the AI chip has become as mission-critical as the drivetrain itself. Electric and autonomous vehicle development is accelerating this further, as both categories depend heavily on AI for optimized real-time performance and safety compliance.

● Broad-Based Industrial AI Adoption Driving Structural Demand

AI adoption has moved well beyond the tech sector. According to IBM, 34% of companies globally already deploy AI in production, while another 42% are actively evaluating it — meaning roughly three-quarters of the corporate world is converging on AI-powered operations. In healthcare, AI chips enable real-time diagnostic imaging and personalized treatment pathways. In finance, they power fraud detection at transaction speed. In retail, demand forecasting and dynamic pricing rely on AI inference chips. AMD reinforced this momentum with its 2024 launch of Instinct MI325X accelerators and 5th Gen EPYC CPUs, delivering scalable AI deployments across enterprise data centers. This multi-sector pull makes AI chip demand structural rather than cyclical.

● Government Policy and Strategic National Investment

AI chip development has become a matter of national economic strategy. The European Chips Act targets doubling the EU’s global semiconductor production share from 10% to 20% by 2030. The U.S. CHIPS and Science Act has directed tens of billions into domestic chip manufacturing. Microsoft’s USD 2.7 Billion investment in Brazil’s AI infrastructure is projected to boost GDP by 4.2% by 2030, while training 5 Million people in AI skills over three years. Saudi Arabia’s Vision 2030 has attracted Groq’s ultra-fast AI chip infrastructure — achieving 534 tokens per second with a developer base exceeding 444,000 — demonstrating how sovereign AI ambitions are converting directly into chip demand at scale.

Artificial Intelligence Chip Market Trends:

● The Push Toward Energy-Efficient AI Silicon

Power consumption has become a defining challenge in AI chip design. Bain & Company’s 2024 Technology Report projects AI workloads to grow 25–35% annually through 2027, pushing infrastructure costs sharply higher and forcing chip designers to rethink architectures. Dynamic voltage scaling, specialized thermal management systems, and task-specific instruction sets are enabling next-generation chips to handle intensive AI workloads while significantly cutting energy use. For hyperscalers running tens of thousands of GPUs, even modest per-chip efficiency improvements translate into hundreds of millions in annual savings. Energy efficiency has moved from a marketing differentiator to a hard commercial requirement in an increasingly competitive AI chip market.

● AI Chips Embedding Deeper into Consumer Electronics

What started in data centers has moved into consumers’ pockets. Smartphones, wearables, smart home devices, and gaming hardware increasingly rely on dedicated on-device AI processing cores to enable real-time voice recognition, computational photography, health monitoring, and personalized recommendations — all without cloud round-trips. India’s electronics sector reaching USD 155 Billion in FY23, nearly doubling from USD 48 Billion in FY17, signals how fast device ecosystems are scaling in high-growth markets. As consumers come to expect their devices to anticipate and respond intelligently, AI chips are becoming non-negotiable in consumer hardware design, driving volumes higher and accelerating cost optimization across the broader supply chain.

● Hyperscalers and AI Labs Moving Toward Custom Silicon

One of the most structurally significant shifts in the AI chip space is the move by large technology companies to design their own chips in-house. OpenAI has partnered with Broadcom and TSMC to build its first proprietary AI chip, targeting reduced dependence on external hardware providers. Amazon is preparing custom cloud AI silicon to address supply crunches and reduce costs for developers. Apple’s Neural Engine has already set an industry benchmark for on-device AI performance. This vertical integration trend is reshaping the competitive landscape — the chip market is no longer just about selling processors to enterprises, it’s about enabling a new class of AI-native chipmakers born entirely from the demands of modern large-scale model training and inference.

Recent News and Developments in the Artificial Intelligence Chip Market

● November 2024: Amazon announced plans to unveil custom AI chips for cloud computing, offering a cost-effective solution for developers and addressing growing concerns about AI chip supply crunches. The chips are expected to broaden accessibility to AI workloads on AWS while reducing reliance on third-party GPU suppliers.

● November 2024: Huawei targeted early 2025 for mass production of its next-generation AI chip, optimized for AI-driven applications. The move reflects Huawei’s commitment to technological self-reliance despite ongoing U.S. trade restrictions, signaling continued geopolitical competition in the global AI chip supply chain.

● October 2024: OpenAI partnered with Broadcom and TSMC to develop its first proprietary AI chip, marking a strategic shift away from full dependence on NVIDIA hardware. The collaboration is aimed at optimizing inference performance for OpenAI’s own model architectures and reducing long-term hardware procurement costs.

● September 2024: Intel launched its latest AI chip lineup targeting enterprise AI applications, with a focus on power-efficient and scalable architectures. The announcement came alongside industry speculation about potential acquisitions, underscoring Intel’s push to remain competitive in a market increasingly dominated by GPU-centric players like NVIDIA.

● August 2024: India’s Krutrim, founded by Ola’s Bhavish Aggarwal, announced its first domestic AI chip — Bodhi 1 — targeting 2026 availability, with a follow-up chip Bodhi 2 (supporting over 10 Trillion model parameters) planned for 2028. Partnering with Arm and Untether AI, Krutrim also plans to scale data center capacity to 1 GW by 2028, signaling India’s serious intent to build a sovereign AI chip ecosystem.

Note: If you require specific details, data, or insights that are not currently included in the scope of this report, we are happy to accommodate your request. As part of our customization service, we will gather and provide the additional information you need, tailored to your specific requirements. Please let us know your exact needs, and we will ensure the report is updated accordingly to meet your expectations.

About the Creator

Rahul Pal

Market research professional with expertise in analyzing trends, consumer behavior, and market dynamics. Skilled in delivering actionable insights to support strategic decision-making and drive business growth across diverse industries.

Steps for Application Integration on AWS

It is neither new nor a secret that modern businesses have come to rely on a massive ecosystem of microservices and third-party SaaS platforms. But to do what exactly, you ask. For starters, to provide seamless digital experiences. Adopting distributed architecture decidedly improves agility and scalability. But there's also a significant challenge, i.e. ensuring independent components can communicate and share data without forming brittle dependencies. Thankfully, an effective solution is found in application integration on AWS. It addresses this issue by providing a managed framework for connecting disparate systems. Organizations can automate business processes while reducing the need for custom "glue" code by using purpose-built services for messaging, workflow orchestration, etc.

By Ryan Williamsonabout 5 hours ago in 01

How One EdTech App Doubled Retention With AI in 90 Days

In the competitive landscape of 2026, the primary challenge for educational platforms is no longer the delivery of content. It is the persistence of the learner. For many developers, AI in EdTech has shifted from a speculative feature to the core engine of user stickiness. This transition is critical because, despite the massive influx of digital learning tools over the last decade, the industry has long struggled with a "completion crisis." The average course completion rate often hovered below 15% for non-mandatory content.

By Del Rosario4 days ago in 01

Comments

There are no comments for this story

Be the first to respond and start the conversation.